Introduction

Michael Bücker

Professor of Data Science at Münster School of Business

The incumbent: Score Cards

Steps for Score Card construction using Logistic Regression (Szepannek 2017)

- Automatic binning

- Manual binning

- WOE/Dummy transformation

- Variable shortlist selection

- (Linear) modelling and automatic model selection

- Manual model selection

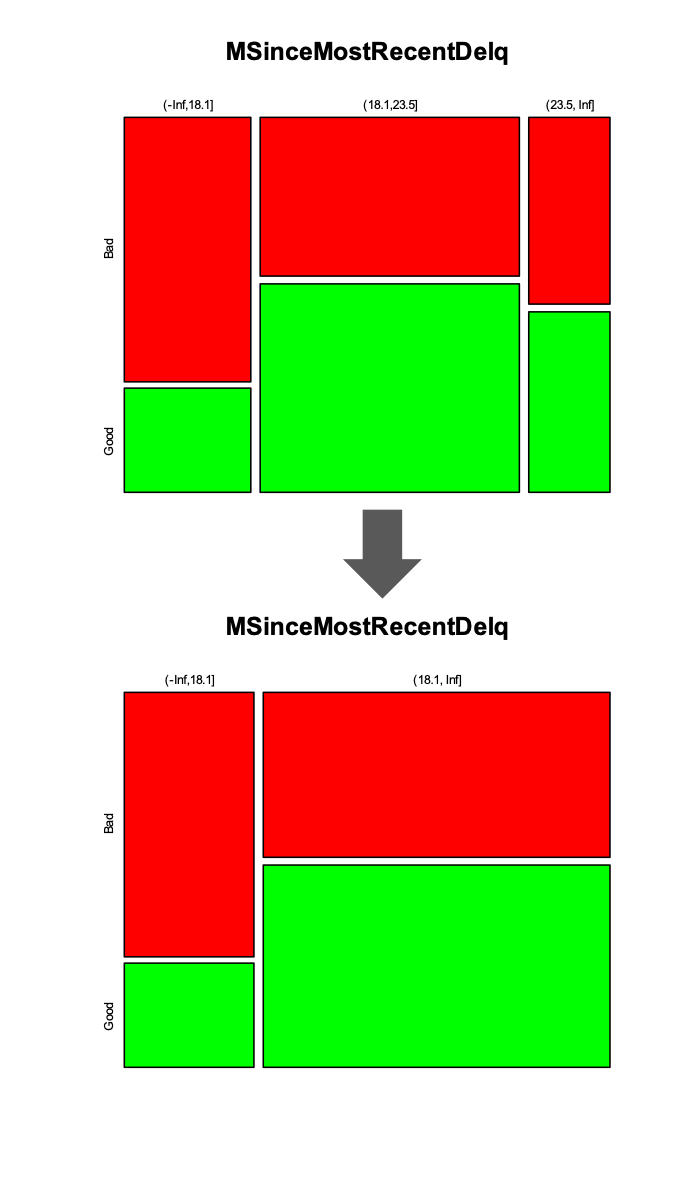

Score Cards: Manual binning

Manual binning allows for

- (univariate) non-linearity

- (univariate) plausibility checks

- integration of expert knowledge for binning of factors

... and means a lot of manual work

Data set for study: xML Challenge by FICO

- Explainable Machine Learning Challenge by FICO (2019)

- Focus: Home Equity Line of Credit (HELOC) Dataset

- Customers requested a credit line in the range of $5,000 - $150,000

- Task is to predict whether they will repay their HELOC account within 2 years

- Number of observations: 2,615

- Variables: 23 covariates (mostly numeric) and 1 target variable (risk performance "good" or "bad")

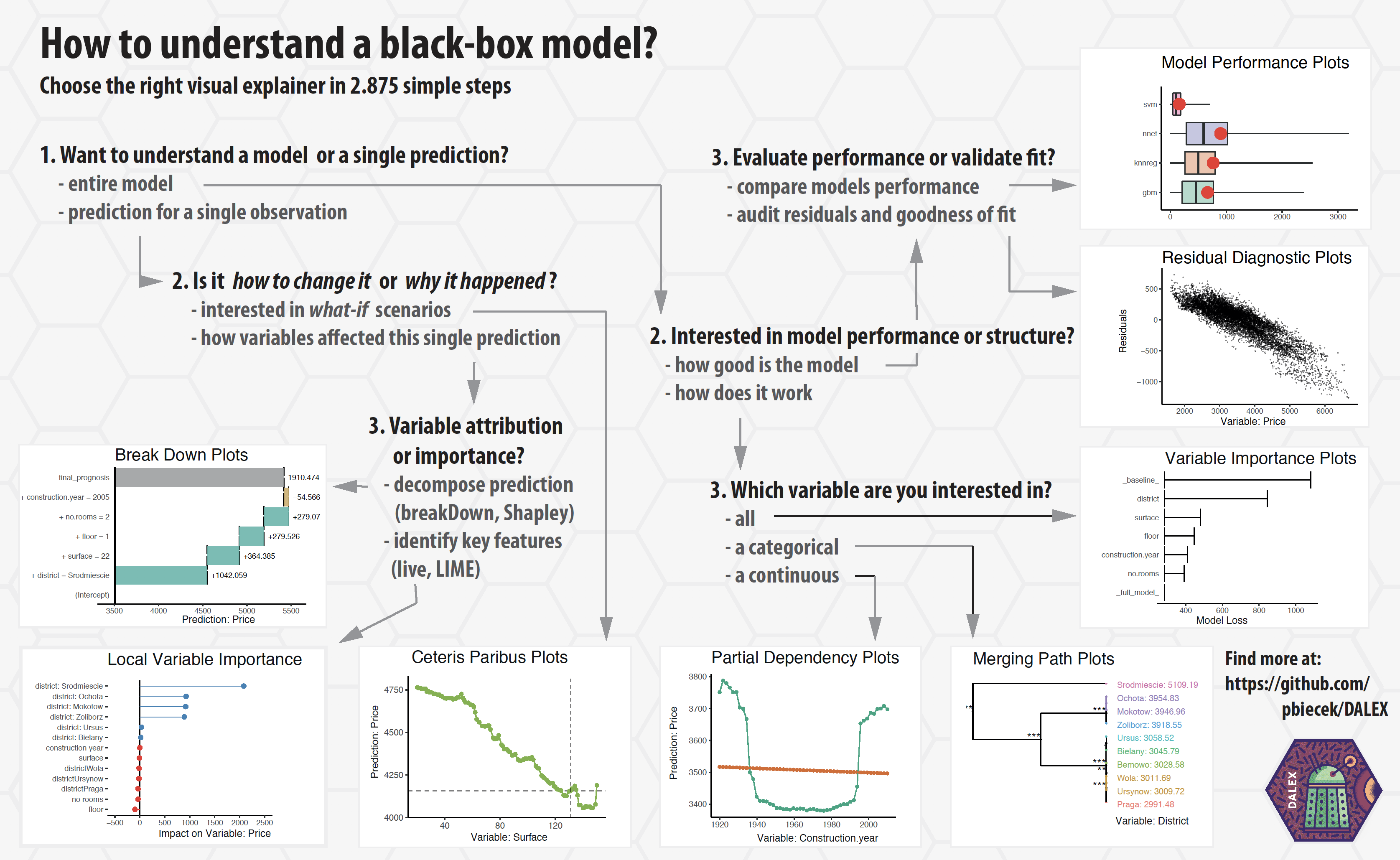

Implementation in R: DALEX

- Descriptive mAchine Learning EXplanations

- DALEX is a set of tools that help to understand how complex models are working

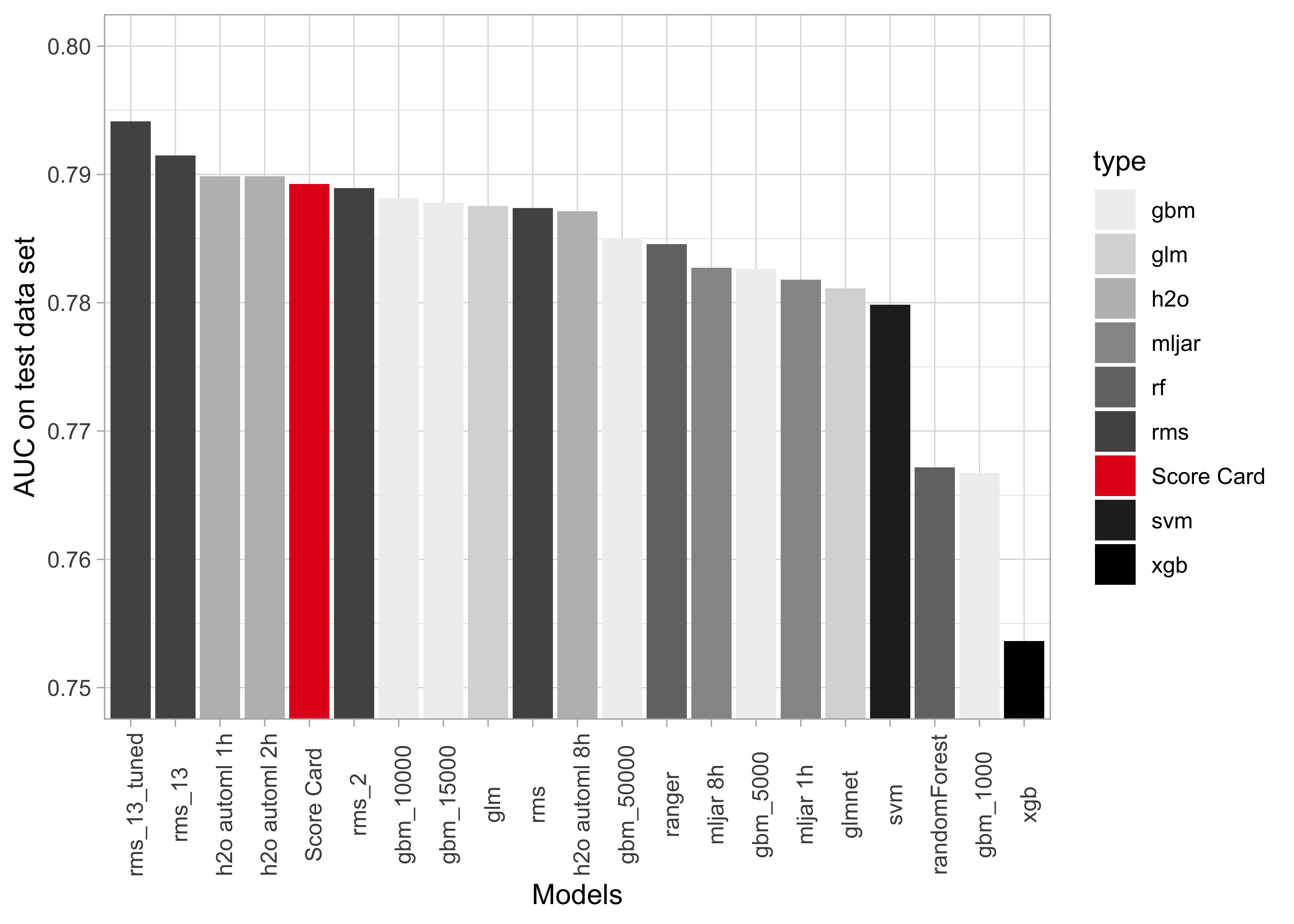

Results: Comparison of model performance

- Predictive power of the traditional Score Card model surprisingly good

- Logistic Regression with spline based transformations best, using

rmsby Harrell Jr (2019)

Results: Comparison of model performance

For comparison of explainability, we choose

- the Score Card,

- a Gradient Boosting model with 10,000 trees,

- a tuned Logistic Regression with splines using 13 variables

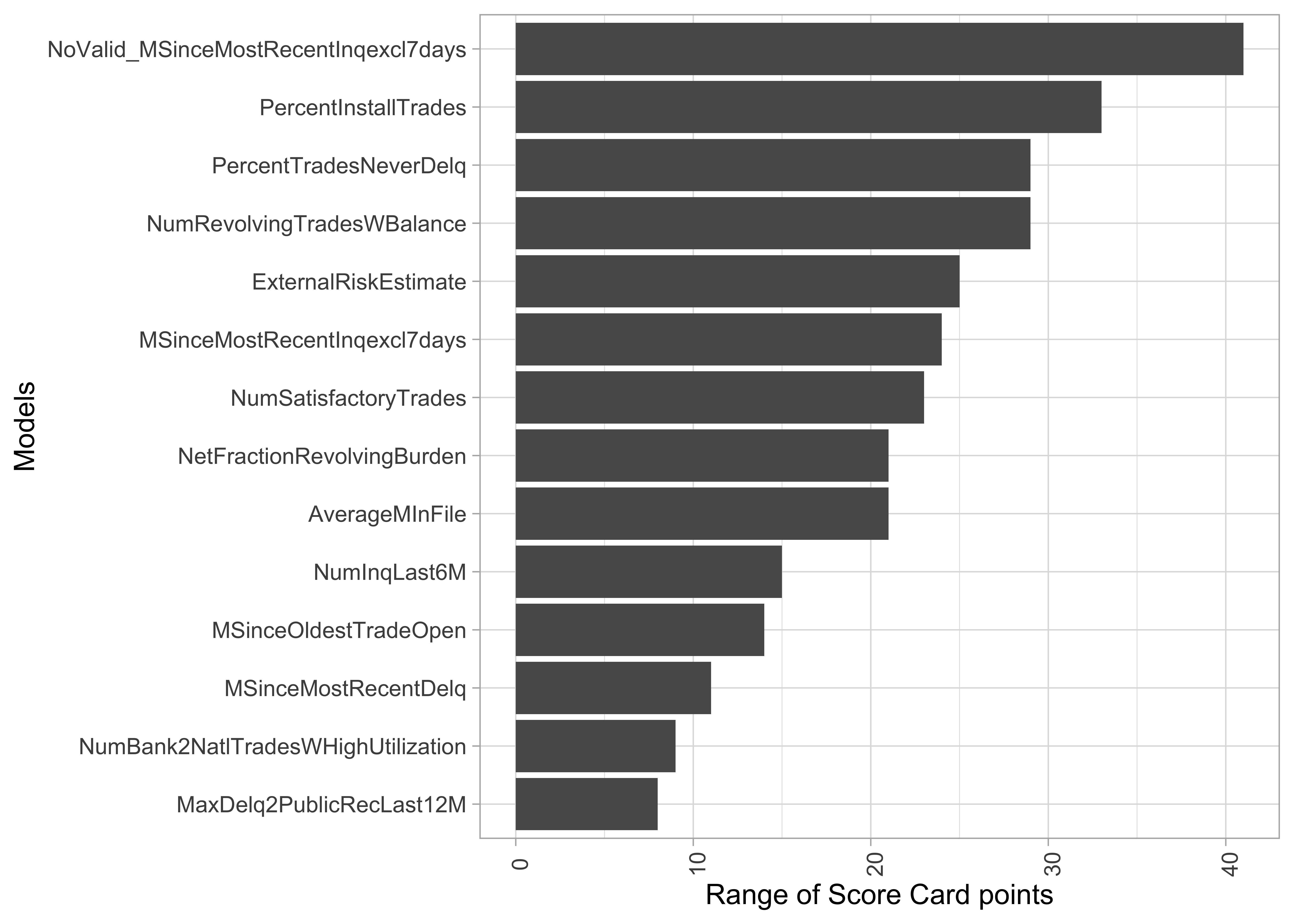

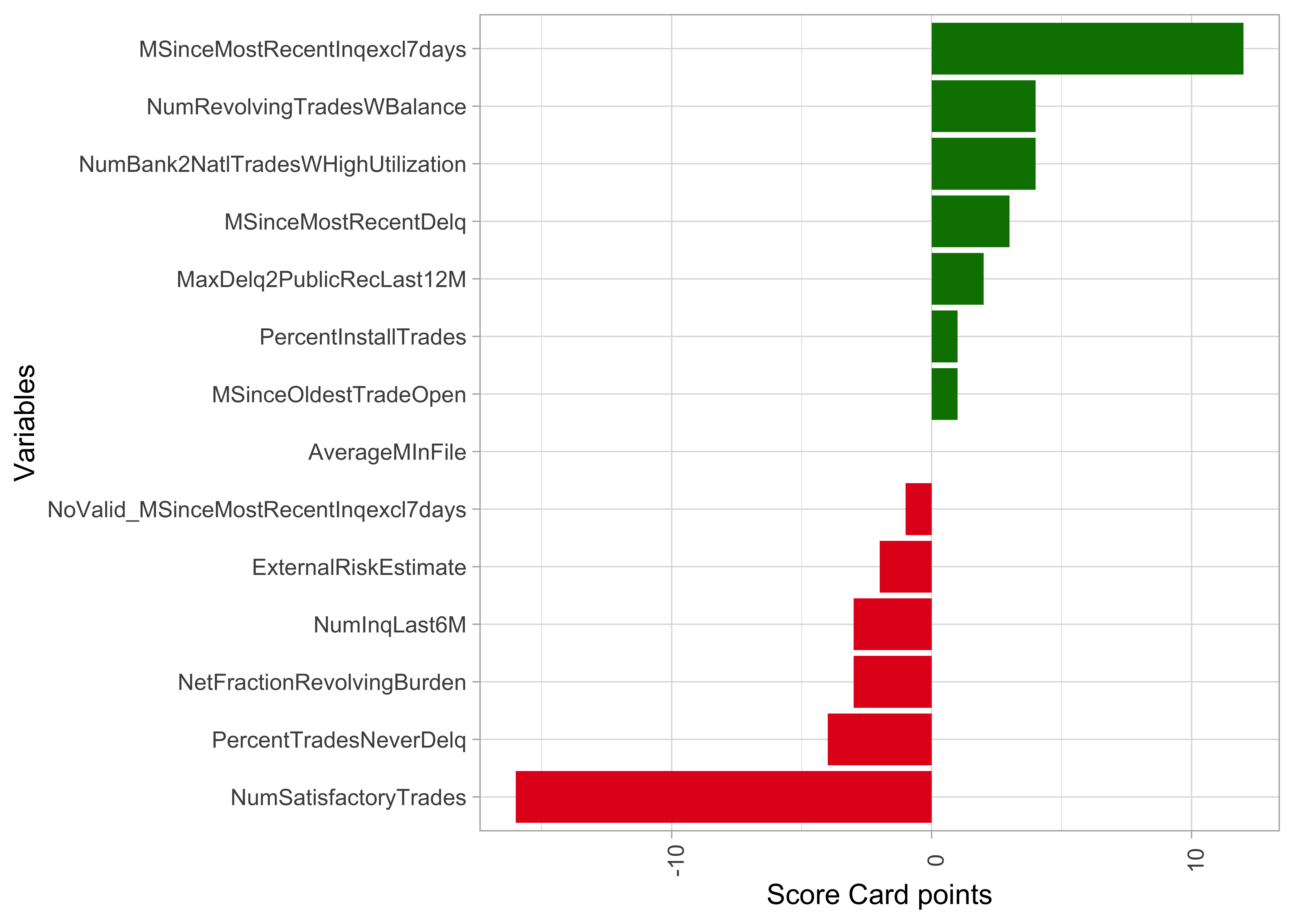

Score Card: Variable importance as range of points

- Range of Score Card point as an indicator of relevance for predictions

- Alternative: variance of Score Card points across applications

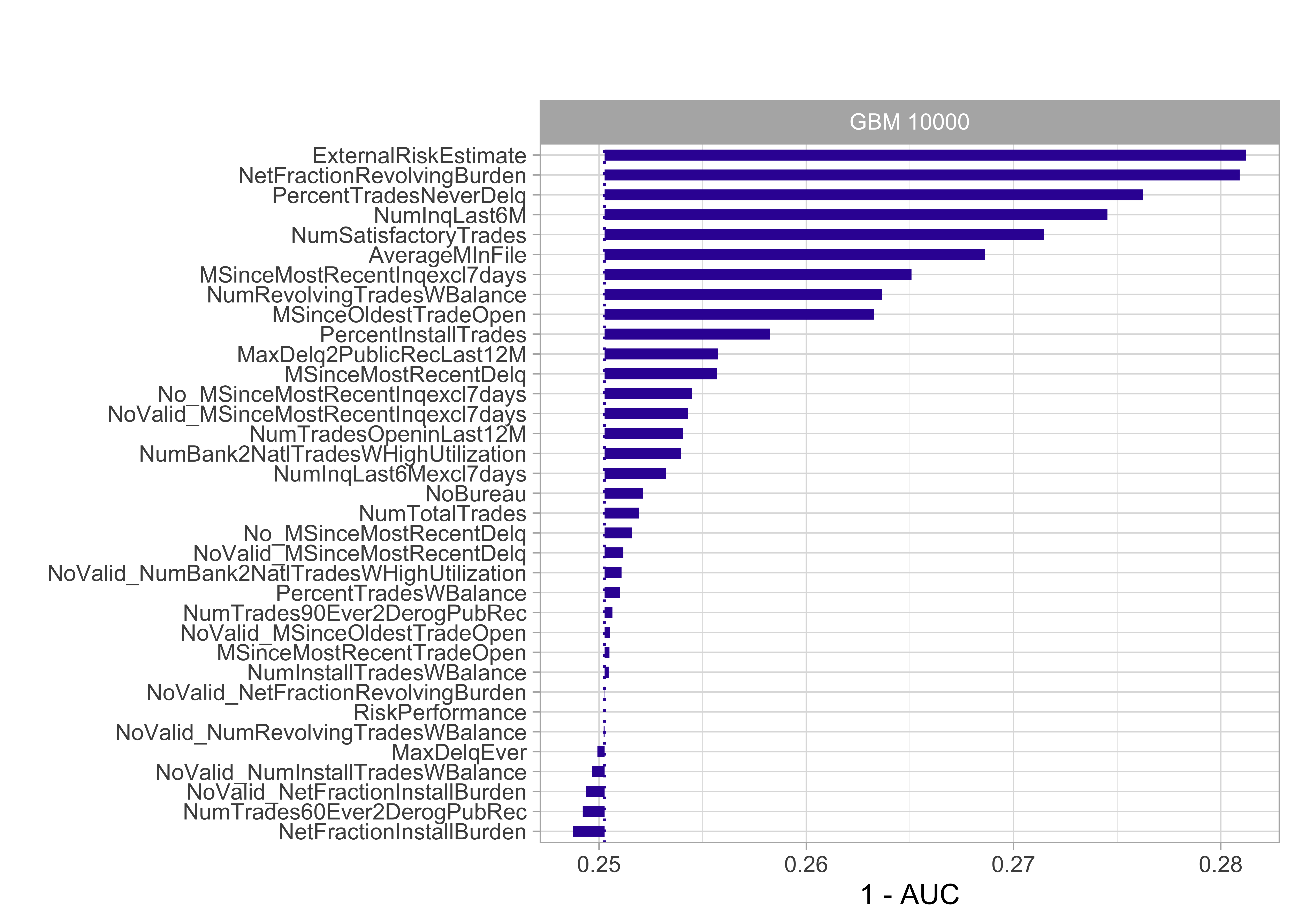

Model agnostic: Importance through drop-out loss

- The drop in model performance (here AUC) is measured after permutation of a single variable

- The more siginficant the drop in performance, the more important the variable

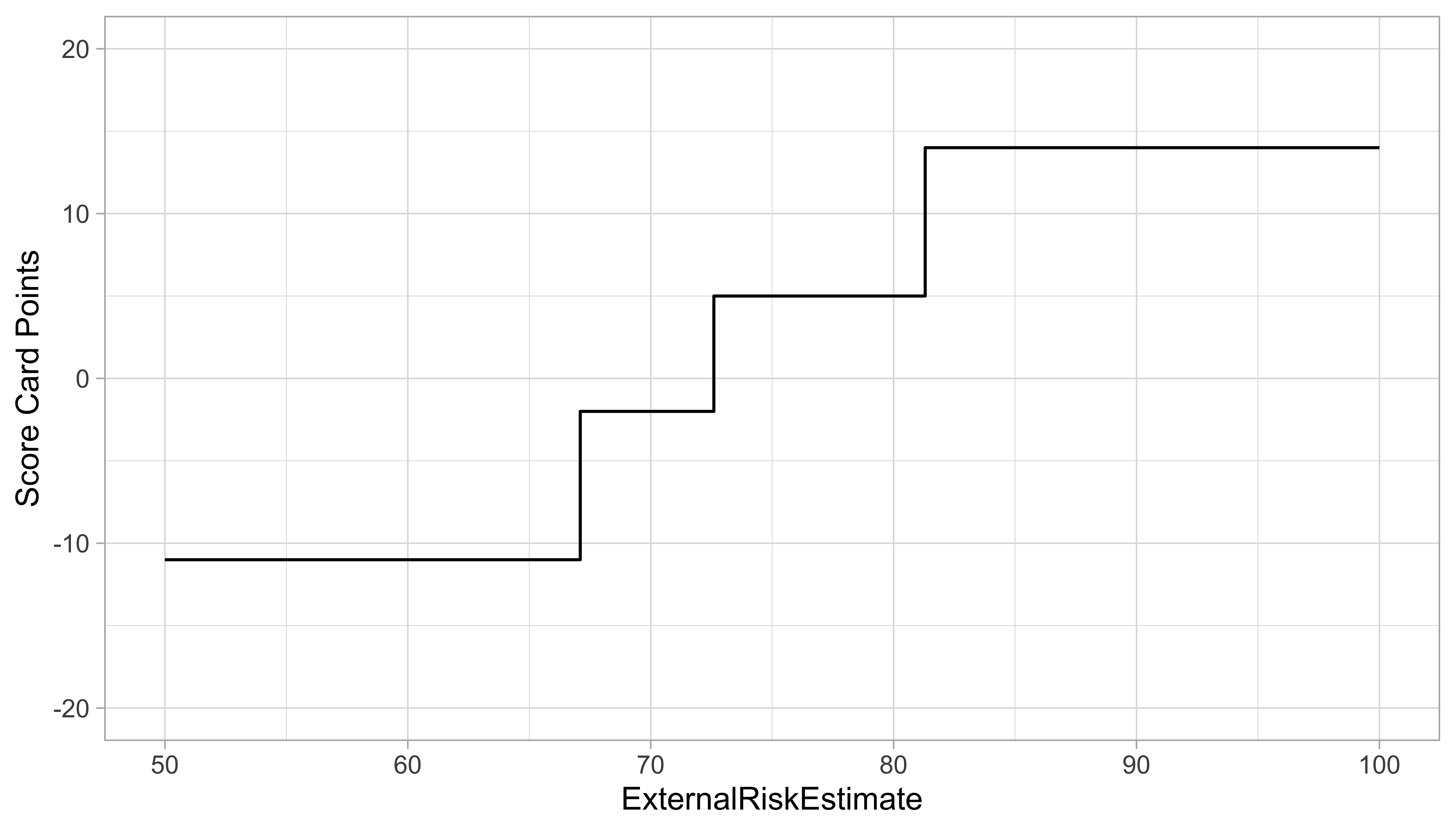

Score Card: Variable explanation based on points

- Score Card points for values of covariate show effect of single feature

- Directly computed from coefficient estimates of the Logistic Regression

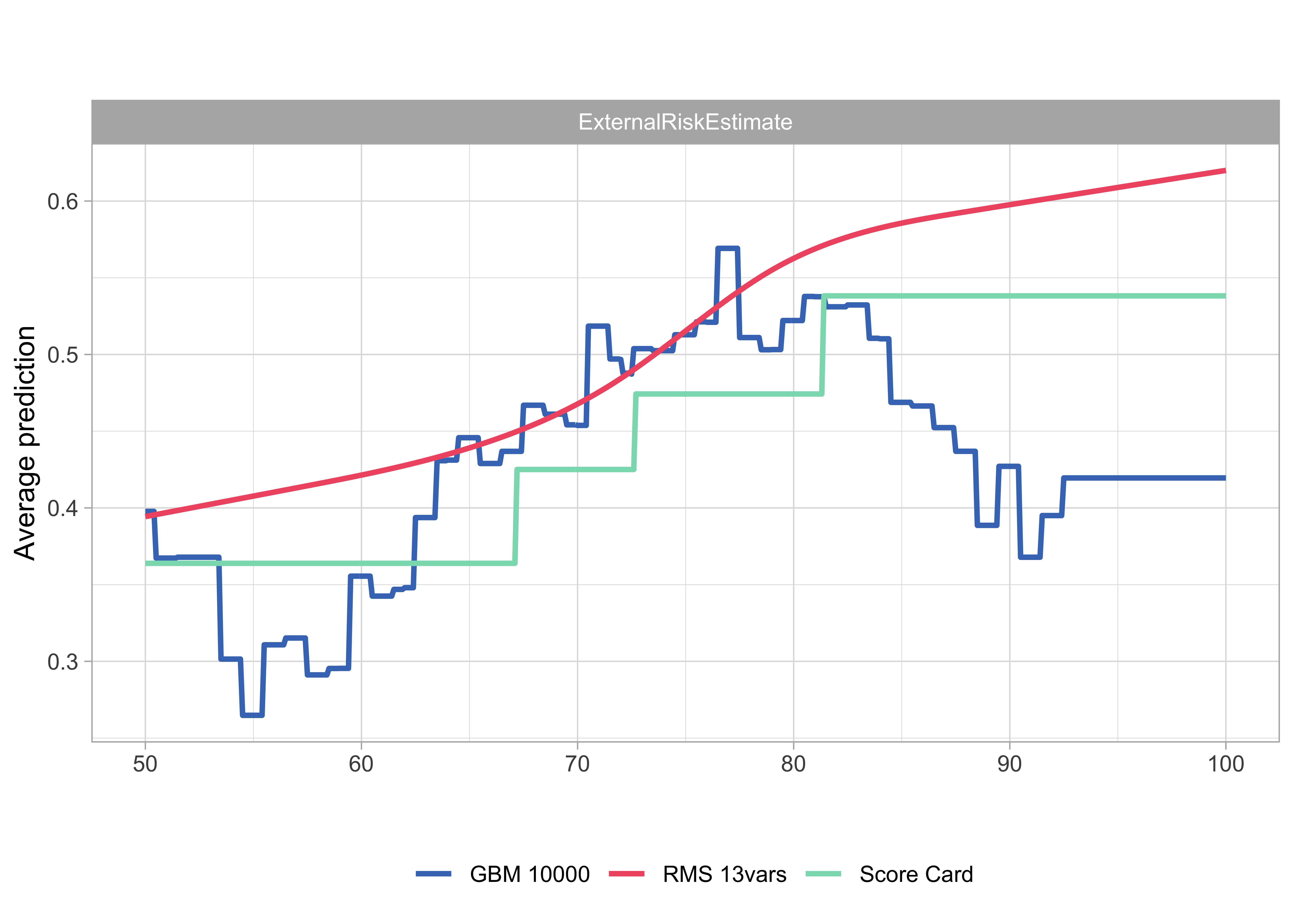

Model agnostic: Partial dependence plots

- Partial dependence plots created with (Biecek 2018)

- Interpretation very similar to marginal Score Card points

Score Card: Local explanations

- Instance-level exploration for Score Cards can simply use individual Score Card points

- This yields a breakdown of the scoring result by variable

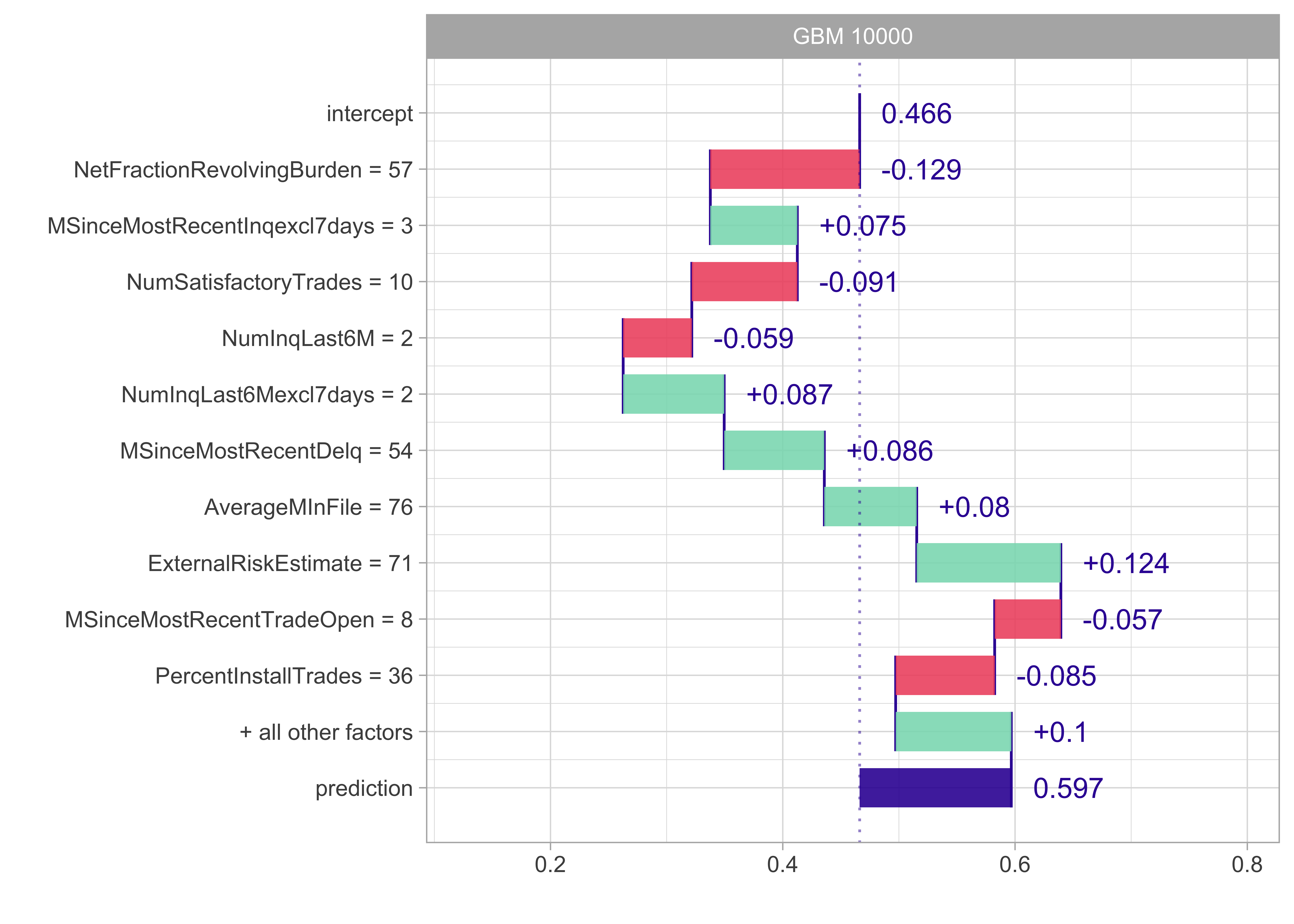

Model agnostic: Variable contribution break down

- Such instance-level explorations can also be performed in a model-agnostic way

- Unfortunately, for non-additive models, variable contributions depend on the ordering of variables

Model agnostic: SHAP

- Shapley attributions are averages across all (or at least large number) of different orderings

- Violet boxplots show distributions for attributions for a selected variable, while length of the bar stands for an average attribution

Thank you!

Prof. Dr. Michael Bücker

Professor of Data Science

Münster School of Business

FH Münster - University of Applied Sciences -

Corrensstraße 25, Room C521

D-48149 Münster

Tel: +49 251 83 65615

E-Mail: michael.buecker@fh-muenster.de

http://prof.buecker.ms